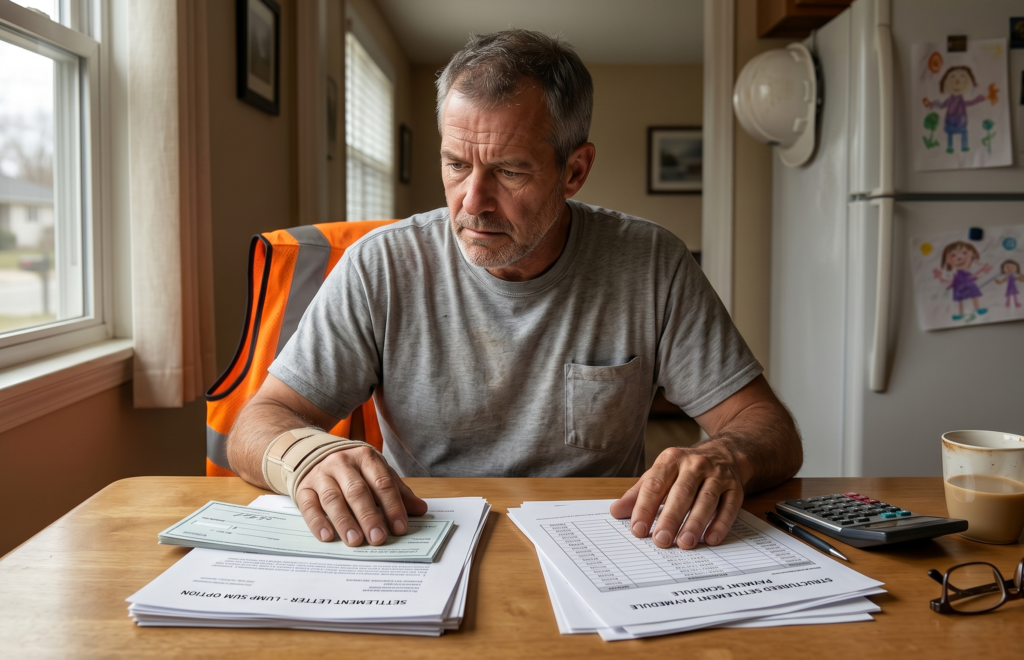

Lump Sum vs. Structured Settlements: Which Is Better for Your Future?

When a workers’ compensation claim moves toward resolution, an injured construction worker is often handed a choice that will shape their finances for years: take the money as one large lump sum, or accept a structured settlement that pays out over time. Both close the claim. But they protect — and expose — a worker in very different ways, and the carrier rarely explains the trade-offs in plain terms.

This article breaks down how each option actually works, who tends to benefit from each, and the quiet details that can turn a fair-looking number into a regret.

What a Lump Sum Settlement Really Means

A lump sum settlement is a single, one-time payment that closes the claim. In exchange for that check, a worker generally gives up the right to come back for more money later — and, in many agreements, the right to future medical care tied to the injury.

Generally, in many states, a lump sum is attractive for clear reasons:

- Immediate access to the full amount, useful for paying down debt that piled up while wages stopped.

- Control over how and when the money is used or invested.

- A clean break from the insurance carrier, with no ongoing claim to manage or defend.

The risk lives in that same freedom. A lump sum has to last as long as the consequences of the injury do — sometimes a lifetime — and once it is spent, there is usually no going back to the carrier for more.

Insurer trick to watch for: A lump sum is sometimes presented as the “simple” option precisely because it lets the carrier close the file and erase future medical exposure in one move. Attorneys often recommend asking, in writing, whether the lump sum closes future medical benefits — because that single clause can be worth more than the check itself.

What a Structured Settlement Really Means

A structured settlement replaces one large payment with a stream of guaranteed payments over a set period — monthly, quarterly, annually, or in scheduled larger installments. It is typically funded through an annuity purchased from an insurance company.

Standard guidelines suggest structured payments tend to favor workers who need long-term stability:

- Predictable income that replaces lost wages on a steady schedule.

- Protection from overspending, since the money cannot all disappear at once.

- Potential tax advantages, as qualifying workers’ comp settlement payments are often treated favorably — though rules vary and a tax professional should confirm any specific situation.

The trade-off is flexibility. A structured plan is difficult to change once signed, and it may not provide enough cash up front for a large, immediate need — a home modification, a vehicle, or clearing high-interest debt.

Lump Sum vs. Structured: A Side-by-Side Look

| Factor | Lump Sum | Structured Settlement |

|---|---|---|

| Access to money | All at once, immediately | Spread out on a fixed schedule |

| Risk of running out | Higher — depends on discipline | Lower — payments are guaranteed |

| Flexibility to change later | Full control after payout | Very limited once signed |

| Best suited for | Large immediate needs, debt payoff | Long-term living expenses, lasting injuries |

| Future medical care | Often closed out — read carefully | May be structured separately |

Which One Fits Which Worker?

There is no universally “better” option — only the option that fits a specific injury, family situation, and state. Generally, in many states, the decision tends to turn on a few honest questions:

- How permanent is the injury? A lasting impairment that limits future earning often pairs better with steady, long-term payments.

- What does the next year demand? Urgent debt or a major one-time cost may call for cash up front.

- How comfortable is the worker managing a large sum? A structure removes the pressure of stretching a single check across decades.

- Is future medical care still likely? Closing that door for a lump sum can be the most expensive part of the deal.

Deadline warning: State laws vary significantly regarding settlement approval, revocation windows, and how future medical benefits may be closed. In some states a worker has only days to reconsider a signed agreement; in others, a judge must approve the terms first. Because a finalized settlement is generally very difficult to undo, attorneys often recommend confirming every applicable deadline and approval step before agreeing to a structure or a lump sum.

The Hybrid Option Many Workers Overlook

The choice is not always all-or-nothing. Standard guidelines suggest that many settlements can be split — a partial lump sum to cover immediate debts and pressing needs, with the remainder structured into guaranteed payments for long-term stability. This hybrid approach can capture the strengths of both while softening the weaknesses of each.

For a broader walk-through of how settlement decisions fit into the wider claims process, our complete guide to construction injury benefits covers each stage in plain language.

Where Official Information Fits In

Settlement pressure often relies on the assumption that a worker doesn’t fully understand their rights or the long-term cost of their injury. Public agencies publish a great deal of free, neutral information. The U.S. Department of Labor’s Workers’ Compensation resource is one authoritative starting point for understanding how these programs are structured.

Pairing that public information with your own medical records and a clear sense of your future needs creates a far stronger foundation than relying on the carrier’s framing alone.

How Workers Typically Approach the Decision

There is no single correct answer, and the right path depends heavily on the injury and the state. That said, attorneys often recommend a measured rather than rushed approach:

- Requesting the full settlement terms in writing, including any language about future medical care.

- Mapping out realistic long-term costs before deciding how much cash is truly needed up front.

- Understanding how the local state system treats settlement taxes and approval before signing.

- Considering whether a hybrid split serves the family better than either extreme.

State laws vary significantly, and a strategy that fits a worker in one state may be entirely wrong in another. Nothing here is legal or financial advice; it is general, informational background to help an injured worker ask better questions.

See What Your Claim May Actually Be Worth First

Before choosing between a lump sum and a structure, it helps to have an independent sense of the range your claim might fall into. HardHat Rights offers a free, anonymous Benefits Estimator that walks through the same value drivers insurers use — medical costs, lost wages, and impairment — without asking for your name or signing you up for anything.

Try the free, anonymous Benefits Estimator at HardHat Rights to see how a settlement offer compares to your real long-term needs — and walk into the lump sum versus structured decision informed instead of pressured.

Disclaimer: This website is for informational purposes only and does not constitute legal or medical advice. The content provided is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Benefit estimates are approximations based on standard state formulas and do not account for your state’s specific caps or your individual circumstances. Always consult a licensed workers’ compensation attorney in your state for legal advice, and a qualified health provider regarding any medical conditions or treatment.