Traumatic Brain Injuries on the Jobsite: When the Hard Hat Isn’t Enough

A hard hat is built to stop a falling bolt or a glancing blow. It was never designed to stop your brain from slamming against the inside of your own skull. That is the hard truth behind a traumatic brain injury, or TBI: the impact that matters most often happens inside the helmet, where no foam liner can reach. A worker can take a fall, get checked at the ER, be told “nothing is broken,” and walk out the door with a brain injury that no one has named yet. Weeks later, the headaches, the lost words, and the sudden flashes of anger arrive, and by then the insurance company may already be calling the case minor.

Here is what few injured workers are told at the start: a TBI is often an invisible injury, and in workers’ compensation, invisible injuries are the ones insurers fight hardest to minimize. Understanding why is the first step toward protecting a claim that can otherwise slip away.

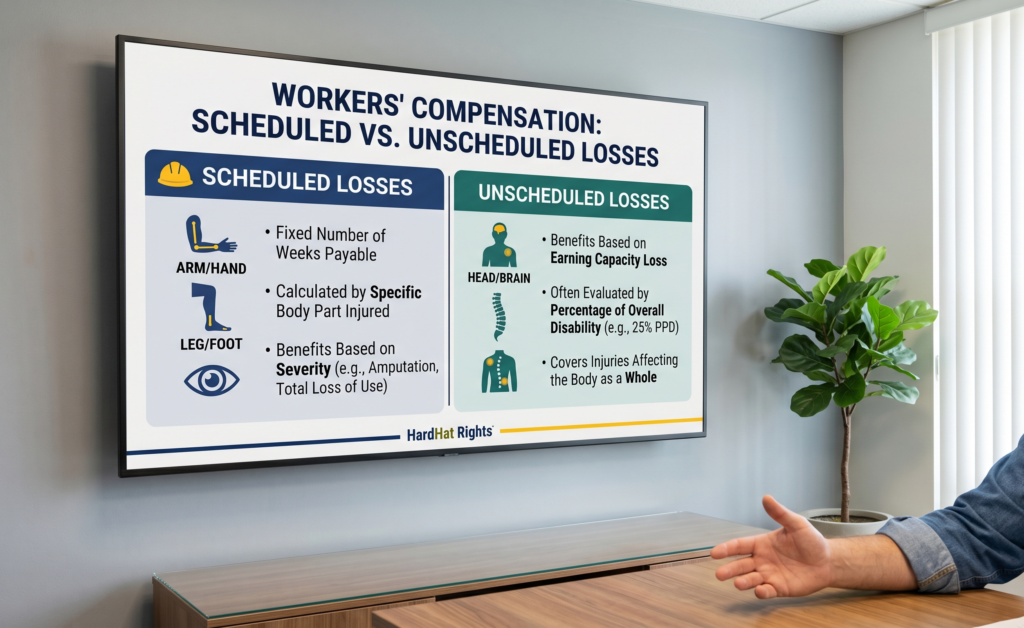

Why a “Mild” TBI Is Anything But Minor

The word doctors often use is concussion, and on paper a concussion is classified as a “mild” traumatic brain injury. That single word does enormous damage to construction claims, because insurers lean on it to suggest the worker simply needs rest and will be fine in a week. The reality on a jobsite is very different.

Construction brain injuries rarely come from a clean, gentle bump. They come from falls from height, struck-by incidents with swinging loads or falling tools, scaffold collapses, and vehicle strikes. According to federal safety data, falls and struck-by events are among the leading causes of serious harm in the trades, and both deliver the exact kind of force that injures the brain.

- Falls from scaffolds, ladders, and roofs. The head can strike a surface or whip violently even without a direct hit.

- Struck-by falling objects. A dropped tool from several stories up carries enough force to injure the brain through the helmet.

- Equipment and vehicle incidents. Forklifts, loaders, and falling materials can cause sudden acceleration injuries.

- Explosions and blasts. Pressure waves alone can cause brain trauma with no visible wound at all.

Insurer tactic to watch for: A common move is to treat any head injury labeled “concussion” or “mild TBI” as a short-term problem that should resolve in days. By anchoring the case to that word early, an insurer can later argue that lingering symptoms must be unrelated, even when the worker has never recovered.

The Symptoms Insurers Hope You Won’t Connect

One of the cruelest features of a brain injury is that the worker is often the last to realize how much has changed. Symptoms can appear hours or even days after the accident, and they are easy to blame on stress, poor sleep, or simply getting older. When those symptoms are never documented and linked to the accident, the claim quietly weakens.

| Symptom Category | What It Can Look Like | Why It Gets Missed |

|---|---|---|

| Cognitive | Memory gaps, trouble focusing, losing words mid-sentence | Blamed on age, stress, or being “distracted” |

| Physical | Persistent headaches, dizziness, light and noise sensitivity | Treated as ordinary tension or migraines |

| Emotional | Sudden anger, anxiety, depression, personality shifts | Mistaken for a “bad attitude” or unrelated mental health |

| Sleep | Insomnia or sleeping far more than usual | Dismissed as a lifestyle problem |

The danger is that these changes are reported to a spouse or a foreman, but never to a doctor in writing. In a workers’ compensation system, a symptom that is not in the medical record often does not exist. The injury is real; the paper trail is what proves it.

How Brain Injury Claims Get Quietly Undervalued

Because a TBI cannot always be seen on a standard scan, these claims attract specific challenges. Recognizing the patterns helps a worker keep them in perspective rather than being caught off guard:

- The “clean scan” argument. A routine CT or X-ray often looks normal after a concussion, and insurers may use that normal image to suggest no real injury occurred, even though many brain injuries do not appear on basic imaging.

- The delayed-symptom gap. When symptoms surface days later, insurers may argue the gap proves the brain injury came from something other than the accident.

- The “pre-existing” angle. Past headaches, prior concussions, or normal aging may be blamed for current cognitive problems.

- The independent exam. A doctor chosen by the insurer may briefly evaluate the worker and conclude the injury has fully resolved.

Deadlines matter. State laws vary significantly regarding how quickly a head injury must be reported and how long a worker has to file. Some states require notice within days of noticing symptoms, which is especially harsh for a TBI whose effects appear late. Missing a state-specific window can quietly end an otherwise strong claim before it is ever heard.

Approaches Injured Workers Commonly Consider

Nothing here is legal or medical advice, but the following reflects how serious brain injury claims are generally navigated. Standard guidelines suggest that the strength of the medical record is what protects the value of a TBI case:

- Reporting every symptom in writing. Generally, in many states, cognitive and emotional changes carry weight only when a treating provider records them and ties them to the accident.

- Asking about specialized evaluation. Standard guidelines suggest that neurologists and neuropsychological testing can document injuries that basic scans miss.

- Keeping a symptom journal. A simple daily record of headaches, memory lapses, and mood changes can help a treating doctor see the full pattern over time.

- Understanding the long-term stakes. Attorneys often recommend treating a TBI as a potentially permanent condition until a specialist confirms otherwise, rather than accepting an early “all clear.”

Federal safety standards do not control these state benefit timelines, but they define what a safe jobsite and proper head protection should look like in the first place. You can review official head-protection and fall-safety standards directly at the U.S. Occupational Safety and Health Administration (OSHA).

For a step-by-step walkthrough of how a construction injury moves from accident to resolution, our complete workers’ compensation guide breaks down each stage in plain language.

Remember: A traumatic brain injury is often invisible on paper, which is exactly why documentation matters more here than almost anywhere else. State laws vary significantly, and the specifics of each diagnosis always matter.

See What Your Brain Injury Claim Could Be Worth

A head injury can change how you think, work, and feel long after the bruises fade, and the pressure to accept that you are “just fine” can be overwhelming when no one can see what is wrong. Before a TBI is written off as a minor concussion, it helps to understand the potential direction and value of the claim. Try the free, anonymous Benefits Estimator at HardHat Rights to get a clearer picture in minutes, with no names and no pressure. Start your free Benefits Estimator here and protect what matters most before anyone decides your injury for you.