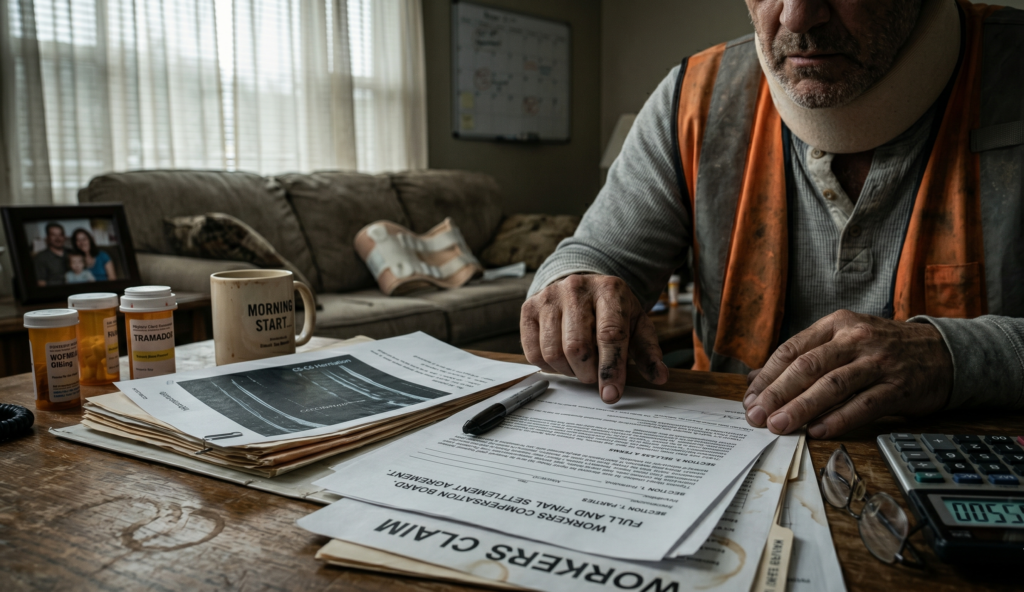

Spinal Cord Injuries and Herniated Discs: Securing Lifetime Medical Benefits

A back injury on a construction site is rarely a single, clean event. It is a herniated disc that flares up months after the fall, the slow loss of feeling in your legs, or the surgeon’s words that change everything: this damage may be permanent. For workers carrying a spinal cord injury, the most important question is not just about today’s treatment. It is whether the system will still cover your care in ten, twenty, or thirty years. That long-term protection is known as lifetime medical benefits, and it is one of the most fiercely contested parts of any serious workers’ compensation claim.

Here is what few injured workers are told at the start: an insurer’s goal is often to close out future medical responsibility as cheaply and as early as possible. Understanding how that happens is the first step toward protecting decades of care.

Why Spinal Injuries Are Treated Differently

Most workplace injuries are expected to heal. A spinal cord injury or a serious herniated disc often does not. Instead, it becomes a lifelong condition that may require ongoing care long after the initial accident. That difference is exactly why these claims draw such intense scrutiny from insurers.

The reason is simple math. The future cost of a permanent spinal condition can be enormous, and it sits on the insurer’s books as an open-ended liability. Several categories of care can extend for years:

- Repeat surgeries. Spinal fusions and disc procedures can fail or require revision over time.

- Pain management. Injections, medication, and specialist visits may continue indefinitely.

- Physical therapy and mobility aids. Ongoing rehabilitation, braces, or assistive equipment.

- Hardware replacement. Implanted devices can wear out and need future revision.

Insurer tactic to watch for: A frequent move is to push for a full and final settlement that “buys out” your future medical care in one lump sum. The offer can look generous on paper, but once you accept and waive future medical rights, the insurer is generally released from paying for that next surgery, even if your spine deteriorates years later.

Open Medical vs. Closed Medical: The Distinction That Defines Your Future

When a serious spinal claim resolves, the single most consequential issue is often whether your medical benefits stay open or are closed forever. The two paths lead to very different futures, and the language used in your paperwork controls which one you get.

| Factor | Open (Lifetime) Medical | Closed Medical Settlement |

|---|---|---|

| Future surgeries | Generally still covered when medically necessary | Typically paid out of your own pocket |

| Long-term risk | Insurer keeps the financial exposure | You absorb the cost of any decline |

| Lump sum offered | Often lower upfront cash | Larger one-time check |

| If your spine worsens | Care channel generally remains available | Reopening can be difficult or impossible |

The trade-off is rarely explained plainly. A larger check feels like a win in a moment of financial pressure, but for a permanent spinal condition, that money can run out long before the medical needs do. Attorneys often describe a closed-out spinal settlement as trading away the most valuable part of the claim for short-term relief.

How Insurers Argue Their Way Out of Lifetime Care

Because the stakes are so high, spinal claims attract specific challenges. Recognizing these patterns helps you keep them in perspective rather than being caught off guard:

- The “pre-existing condition” angle. Many adults have some degree of disc wear, so insurers may argue your herniation existed before the accident. This is one of the most common defenses against spinal claims.

- The paper review. A doctor who has never examined you may review your file and label future surgery “not medically necessary.”

- The MMI label. Once you reach maximum medical improvement, insurers often push to convert ongoing care into a one-time payout.

- The degenerative argument. Future flare-ups may be blamed on natural aging rather than the workplace injury.

Deadlines matter. State laws vary significantly regarding how long medical benefits can stay open and whether a closed claim can ever be reopened. In some states a spine claim can be reopened within a set number of years if the condition worsens; in others, a signed settlement is final and permanent. Missing a state-specific window can quietly end your right to future care.

Approaches Injured Workers Commonly Consider

Nothing here is legal or medical advice, but the following reflects how serious spinal claims are generally navigated. Standard guidelines suggest that the strength of your medical record is what protects long-term care:

- A clear causation link. Generally, in many states, a detailed note from a treating surgeon connecting the herniation or spinal damage directly to the workplace accident is considered the foundation of the claim.

- Documenting the permanence. Imaging, surgical reports, and specialist opinions that describe the condition as lasting help counter the “you’ve healed” argument.

- Understanding what a settlement waives. Attorneys often recommend reading exactly which future rights a lump sum gives up before anything is signed.

- Knowing your state’s rules. Because reopening rights and time limits differ so dramatically, the specific law of your state is generally treated as decisive.

Federal safety standards do not control these state benefit timelines, but they define what a safe jobsite and a properly documented injury should look like in the first place. You can review official fall-protection and worker-safety standards directly at the U.S. Occupational Safety and Health Administration (OSHA).

For a step-by-step walkthrough of how a construction injury moves from accident to resolution, our complete workers’ compensation guide breaks down each stage in plain language.

Remember: Lifetime medical benefits are usually the most valuable and most targeted part of a spinal claim. Once future care is signed away, it can be nearly impossible to recover. State laws vary significantly, and the specifics of your diagnosis always matter.

See What Your Spinal Claim Could Be Worth

A permanent back or spinal cord injury reshapes your future, and the pressure to accept a quick settlement can be overwhelming when bills are piling up. Before you trade away your right to future medical care, it helps to understand the potential direction and value of your claim. Try the free, anonymous Benefits Estimator at HardHat Rights to get a clearer picture in minutes, with no names and no pressure. Start your free Benefits Estimator here and protect what matters most before you sign anything.

Disclaimer: This website is for informational purposes only and does not constitute legal or medical advice. The content provided is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Benefit estimates are approximations based on standard state formulas and do not account for your state’s specific caps or your individual circumstances. Always consult a licensed workers’ compensation attorney in your state for legal advice, and a qualified health provider regarding any medical conditions or treatment.