How Your Average Weekly Wage (AWW) Is Calculated — And How Insurers Shortchange You

Almost every dollar of a workers’ compensation claim — the weekly checks while a construction worker is off the job, and often the final settlement — is built on a single number: the Average Weekly Wage, or AWW. If that number is set too low, every benefit calculated from it is too low as well. Yet the AWW is one of the most commonly understated figures on a claim, and most injured workers never see the math behind it.

This article breaks down how the AWW is normally calculated, the parts of a construction paycheck that carriers conveniently leave out, and the warning signs that the wage figure on your claim may have been quietly trimmed.

What the Average Weekly Wage Actually Is

The AWW is meant to represent what a worker truly earned, on average, before the injury — the baseline a state uses to decide how much wage-replacement to pay. Generally, in many states, the AWW is found by taking gross earnings over a defined look-back period and dividing by the number of weeks in it.

The most common look-back period is the 52 weeks immediately before the date of injury, though this varies. Some states use 13 or 26 weeks; others use the worker’s employment history if it is shorter than a full year. Once the AWW is set, the weekly check is usually a percentage of it — frequently around two-thirds (66.6%) of the AWW, again subject to wide state-by-state differences and a statutory maximum.

Why this number matters so much: The AWW is multiplied across the entire life of a claim. A wage figure that is understated by even $150 a week can compound into thousands of dollars in lost benefits over the months — or years — a serious injury keeps a worker off the job.

The Standard Calculation, Step by Step

While the exact formula differs by state, the general structure most systems follow looks like this:

- Identify the look-back period (commonly the 52 weeks before the injury).

- Add up total gross earnings during that period — before taxes, and ideally including more than just base hourly pay.

- Divide that total by the number of weeks in the period to reach the AWW.

- Apply the state’s benefit percentage (often around two-thirds) to set the weekly compensation rate.

The arithmetic looks simple. The dispute is almost never about the division — it is about what gets counted as earnings in step 2. That is where money goes missing.

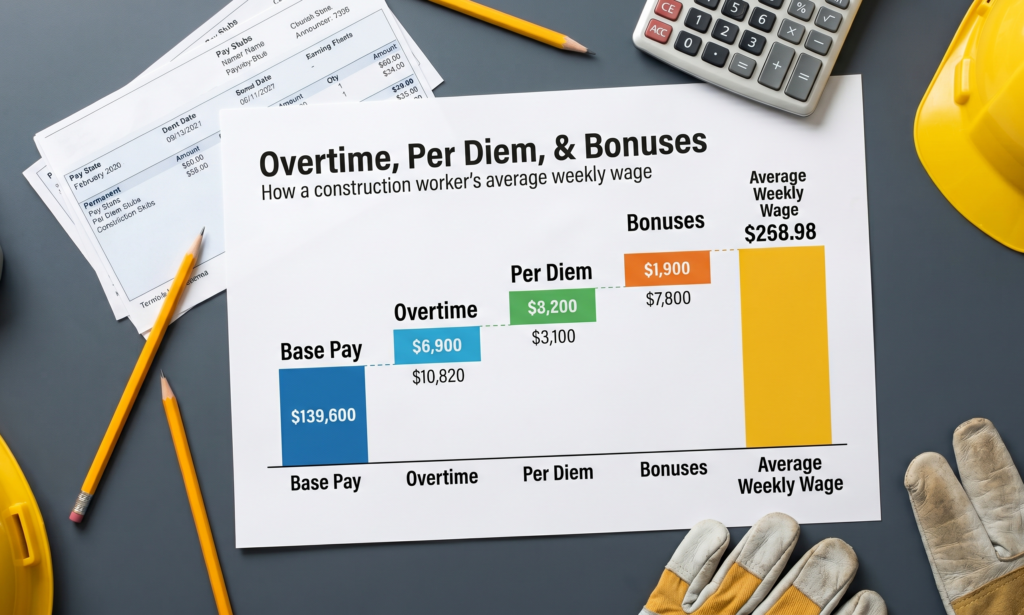

How Insurers Shortchange the Number

Construction pay is rarely just a flat hourly rate. It moves with overtime, seasonal hours, second jobs, and project-based extras. Each of those moving parts is an opportunity for a carrier to calculate a lower AWW — and a worker who only checks the base rate may never notice.

Standard guidelines suggest the AWW should reflect true earning capacity, not a stripped-down version of it. Here are the categories most often left out:

| Often excluded by the carrier | Why it frequently belongs in the AWW |

|---|---|

| Overtime pay | For trades that routinely work 50–60 hour weeks, overtime is real, recurring income — not a bonus. |

| Per diem / travel allowances | In many states, regular per diem that functions as wages may be includable rather than ignored. |

| Bonuses and incentive pay | Recurring production or safety bonuses can form part of true average earnings. |

| Second job / concurrent employment | Several states allow wages from a second job to be combined into one AWW. |

| The value of fringe benefits | Some systems count the lost value of employer-paid health insurance or lodging. |

Insurer trick to watch for: A common tactic is to base the AWW on a single recent pay stub from a slow week, or to use only base hourly pay while quietly dropping overtime and per diem. Attorneys often recommend requesting a full year of earnings records and comparing the carrier’s figure line by line.

The “Short Tenure” Trap

Workers who were recently hired, or who work seasonally, are especially exposed. If a carrier divides a few weeks of low early-season earnings across a full period, the resulting AWW can look far below what the worker would realistically have earned over a normal year.

Generally, in many states, the law provides alternative methods for these situations — such as using the wages of a comparable worker in the same trade, or annualizing seasonal earnings — precisely so a short or interrupted work history does not unfairly sink the number. Whether those methods apply, and exactly how, depends heavily on the state.

For a broader walk-through of how the wage figure connects to the rest of the claims process, our complete guide to construction injury benefits covers each stage in plain language.

Red Flags That Your AWW May Be Too Low

No single sign proves the number was understated, but several together are worth a closer look:

- The weekly check feels far smaller than two-thirds of your normal take-home pay for a busy week.

- The carrier never asked for a full year of pay records.

- Your overtime or per diem appears nowhere in their figure.

- You held a second job that was never mentioned.

- The AWW was based on a slow stretch of work rather than a representative period.

Where Official Wage and Safety Data Fits In

Understated wage figures often rely on a worker not knowing what their trade typically earns or what protections exist. Public agencies publish a great deal of free wage and safety information. The federal OSHA Workers’ Rights resource is one authoritative starting point for understanding the obligations employers carry on a jobsite, and many state labor departments publish prevailing wage data for construction trades.

Pairing that public information with your own pay stubs and tax records creates a far stronger basis for checking the AWW than relying on the carrier’s number alone.

How Workers Typically Verify the Number

There is no single correct path, and the right one depends on the state and the trade. That said, attorneys often recommend a methodical approach rather than accepting the figure at face value:

- Gathering all pay records — ideally a full 52 weeks, including overtime and per diem.

- Asking the carrier in writing exactly how the AWW was calculated and what period it used.

- Listing any concurrent employment that may be combinable in that state.

- Checking whether a seasonal or short-tenure method should have applied instead.

State laws vary significantly regarding the look-back period, which earnings count, and the deadlines to dispute a wage rate — in some states that window is measured in days, not months. Nothing here is legal or financial advice; it is general, informational background to help an injured worker ask better questions.

See What Your Benefits May Actually Be Worth

Before accepting any weekly rate, it helps to have an independent sense of where your AWW — and the benefits built on it — should realistically land. HardHat Rights offers a free, anonymous Benefits Estimator that walks through the same wage and value drivers insurers use, without asking for your name or signing you up for anything.

Try the free, anonymous Benefits Estimator at HardHat Rights to see how your weekly check compares to what your real earnings suggest — and walk into your next conversation with the carrier informed instead of shortchanged.

Disclaimer: This website is for informational purposes only and does not constitute legal or medical advice. The content provided is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Benefit estimates are approximations based on standard state formulas and do not account for your state’s specific caps or your individual circumstances. Always consult a licensed workers’ compensation attorney in your state for legal advice, and a qualified health provider regarding any medical conditions or treatment.