Personal Injury and Workers’ Comp: How the Two Claims Combine for Total Recovery

Most injured construction workers are handed a single claim and told that is the end of the conversation. Workers’ comp pays a slice of the wages, covers approved medical care, and the file is closed. What rarely gets explained is that a serious jobsite injury can sometimes trigger two separate legal claims at the same time — a workers’ comp claim and a personal injury claim — and that the real money is often found in how those two are coordinated, not in either one alone.

This is the part of the system that quietly determines whether an injured worker walks away with a partial check or a recovery that reflects the full cost of what happened. Understanding where these two tracks meet is one of the most valuable things a construction worker can learn after an accident.

Two Different Systems, Two Different Purposes

Workers’ comp and personal injury law were built to do different jobs, and that difference is the entire reason combining them can be so powerful.

Workers’ compensation is a no-fault system. It does not ask who caused the accident. In exchange for that speed and certainty, it generally limits what it pays and, in most states, blocks a worker from suing their own employer. Personal injury law works the opposite way: it requires proof that someone was at fault, but in return it can pursue the full range of damages the law allows — including categories workers’ comp simply does not pay.

The key insight: Workers’ comp limits your claim against your employer. It generally does not limit a personal injury claim against a different party whose negligence helped cause the harm. That gap is where total recovery is built.

Where the Two Claims Overlap

A personal injury claim usually becomes possible when someone other than the direct employer contributed to the accident. On a busy construction site, that list is often long. Parties that commonly come under review include:

- Equipment manufacturers, when a defective machine, tool, ladder, or part fails during normal use.

- General contractors or other subcontractors, when a crew the worker does not work for creates a hazard.

- Property owners, in certain cases involving known dangers or unsafe premises.

- Drivers and trucking companies, when a vehicle is involved while the worker is on the job.

- Maintenance and service firms, when neglected upkeep leads to a failure.

When one of these outside parties is involved, the worker may be able to collect no-fault comp benefits right away while also pursuing a fault-based personal injury claim for everything comp leaves behind.

What Each Claim Actually Pays

The financial reason to look at both claims together is simple: they recover fundamentally different things. Seeing them side by side makes the gap obvious.

| Type of Loss | Workers’ Comp | Personal Injury Claim |

|---|---|---|

| Medical bills | Generally covered (approved care) | Yes, including future treatment |

| Lost wages | Usually a partial percentage | Potentially full lost earnings |

| Future earning capacity | Limited and formula-based | Often recoverable in full |

| Pain and suffering | Generally not available | Often recoverable |

| Loss of quality of life | Not paid | Potentially recoverable |

| Fault required | No — benefits are no-fault | Yes — negligence must be shown |

Attorneys often describe the two as running on parallel tracks. Comp keeps a household afloat in the short term; the personal injury claim pursues the larger human and financial losses comp was never designed to address.

The Trap That Quietly Shrinks Total Recovery: The Comp Lien

Here is where many workers lose money without realizing it. When a personal injury claim succeeds, the workers’ comp insurer that already paid medical bills and wage benefits may be entitled to be repaid out of that recovery. This repayment right is called a lien or subrogation interest, and if it is ignored until the end, it can swallow a large share of the settlement.

This does not make a personal injury claim pointless — it makes timing and strategy everything. Because the lien reaches back into the comp benefits already paid, the two claims generally need to be evaluated together from the start rather than treated as unrelated files. How the lien is calculated, negotiated, and reduced is highly state-specific.

Insurer tactic to watch for: A comp insurer may stay quiet while benefits are paid, then assert the largest possible lien once a personal injury settlement appears. When the lien is addressed only at the finish line, the worker’s net recovery can shrink dramatically. Attorneys often emphasize that coordinating the two claims early is what protects the final number.

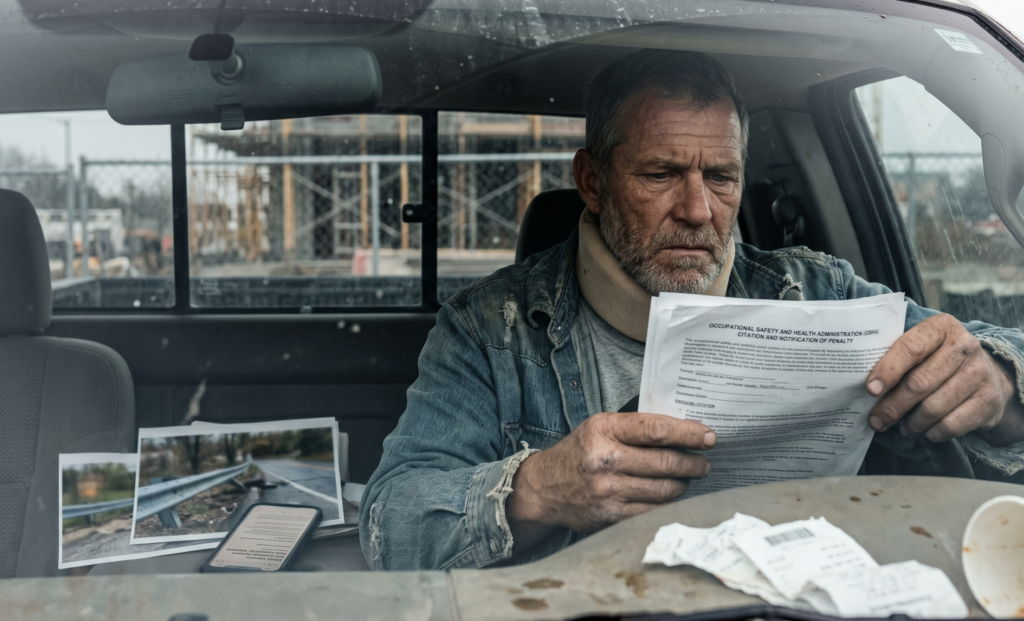

How Safety Violations Strengthen the Personal Injury Side

A personal injury claim rarely succeeds on hardship alone. It is generally built on whether a recognized safety standard was broken. Construction is one of the most heavily regulated industries in the country, and those federal rules create a clear baseline for what responsible companies are expected to do.

When equipment lacked a required guard, when a lift was overloaded, or when a known hazard went unaddressed, that violation can become strong evidence of negligence. The federal safety standards that contractors and manufacturers are expected to follow are published and enforced by the U.S. Occupational Safety and Health Administration (OSHA).

Different Deadlines on Different Clocks

One of the most damaging mistakes is assuming both claims share a single deadline. They do not. The window to report a comp injury may be measured in days, while the window to file a personal injury claim — the statute of limitations — is generally measured in years. Missing either one is usually permanent.

State laws vary significantly. Reporting windows, filing deadlines, lien reduction rules, and shared-fault standards change dramatically from one state to the next. In some states, fault assigned to the injured worker can reduce or even eliminate a recovery; in others, the rules are far more forgiving. Standard guidelines suggest confirming the specific deadlines and rules that apply where the injury occurred, because a closed window generally cannot be reopened.

For a step-by-step walkthrough of how a construction injury moves from the first report all the way to a full resolution, our complete workers’ compensation guide explains each stage in plain language.

Approaches Injured Workers Commonly Consider

While nothing here is legal or medical advice, the following reflects how serious construction injuries with a possible personal injury angle are generally navigated. Attorneys often recommend treating coordination between the two claims as the priority:

- Identifying every company on site. Because fault is frequently shared, knowing which firms were present helps reveal whether a personal injury claim exists at all.

- Mapping the comp lien early. Understanding what the comp insurer may try to recover changes how a personal injury settlement is valued from day one.

- Keeping both claims consistent. Statements made in a comp claim can affect the personal injury case, so aligning them is generally considered important.

- Acting within the deadlines. Because the clocks differ and state rules vary, understanding local time limits early is widely regarded as essential.

Remember: A construction injury can open two doors, not one. Workers’ comp delivers fast, no-fault support, while a personal injury claim may capture the larger losses comp leaves on the table — but the comp lien means the two must be handled together to protect the total. State laws vary significantly, and the specific facts of the jobsite always matter.

See What Your Total Recovery May Be Worth

If a comp check is barely covering the bills, it is worth knowing whether a second claim was sitting in plain sight the whole time — and how much of it you would actually keep after the lien. Far too many construction workers settle for a fraction of what their situation may be worth, simply because no one explained how the two claims fit together. Before assuming workers’ comp is the end of the story, get a clearer picture of the potential value and direction of your case. Try the free, anonymous Benefits Estimator at HardHat Rights — no names, no pressure, just a clearer sense of your options in minutes. Start your free Benefits Estimator here and find out what your total recovery could look like.