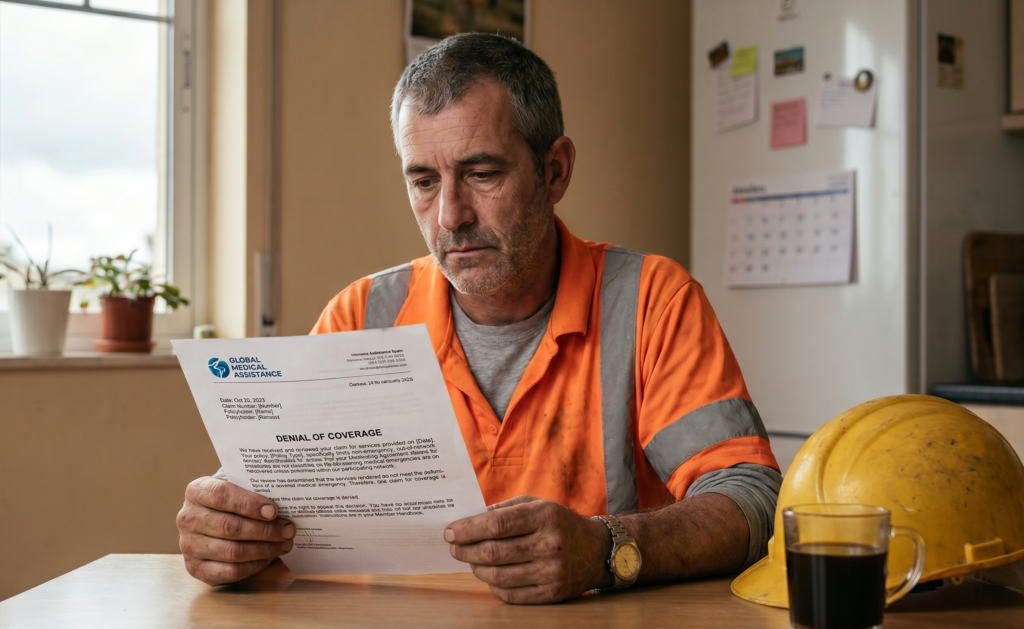

Pre-Existing Conditions: The #1 Excuse Insurers Use to Deny Construction Claims

You hurt your back lifting on the jobsite. The pain is real, the timing is clear, and you filed your claim. Then the denial letter arrives with two words that seem to erase everything: “pre-existing condition.” For injured construction workers, this is the single most common reason insurers give for cutting off benefits, and it is also one of the most widely misunderstood.

Here is what almost no one explains: a prior injury, an old surgery, or even normal wear-and-tear in your spine does not automatically disqualify you from workers’ compensation. In many states, the law was written with exactly this situation in mind.

Why Insurers Reach for the “Pre-Existing” Label So Often

Construction is hard on the body. After years of lifting, climbing, and repetitive strain, very few workers have a “perfect” medical history. Insurers know this. When they pull your old medical records, they are frequently looking for any prior mention of the same body part, even a minor complaint from a decade ago.

The strategy is simple: if they can argue your pain comes from an old problem rather than a recent workplace injury, they may be able to deny the claim entirely or sharply reduce what they pay. Attorneys often describe this as shifting the blame from the jobsite to your past.

Insurer tactic to watch for: A single line in a years-old doctor’s note, such as “occasional lower back stiffness,” can be presented as proof that your current injury is “not work-related.” One sentence, taken out of context, is sometimes treated as if it settles the entire claim.

The Legal Idea That Often Protects You: Aggravation

This is the part insurers rarely highlight. In many states, the law draws a critical distinction between causing an injury and aggravating one. Generally, if a workplace incident makes an existing condition worse, accelerates it, or turns a manageable problem into a disabling one, that aggravation may itself be a compensable injury.

There is also a long-standing legal principle attorneys frequently reference, sometimes called the “eggshell” rule: an employer generally takes a worker as they find them. In plain terms, the fact that your body was more vulnerable to injury does not automatically excuse the employer’s insurer from covering a work-related aggravation.

- New injury: A condition that did not exist before the workplace incident.

- Aggravation: An older condition made measurably worse by work.

- Recurrence: A genuine flare-up of an old injury with no new workplace cause, which is generally harder to claim.

The difference between these categories is where most disputes live, and it is rarely as obvious as an insurer suggests.

Denial vs. Reality: A Quick Comparison

| What the Insurer Says | What the Law Often Recognizes |

|---|---|

| You had back problems before. | A work injury that worsens an old condition may still be covered. |

| This is just normal aging/degeneration. | Work that accelerates degeneration can qualify as an aggravation. |

| Your old records prove it isn’t work-related. | The key question is what changed after the workplace incident. |

| You never reported pain here before. | A previously stable condition becoming disabling can be compensable. |

How These Denials Actually Happen

The denial is rarely a dramatic accusation. More often it is built quietly from your own paperwork. Insurers commonly rely on a few recurring moves:

- Mining old medical records. Any prior reference to the injured body part may be flagged, no matter how minor or how long ago.

- Leaning on an IME opinion. An insurer-selected exam may conclude your symptoms reflect “pre-existing degenerative changes” rather than a workplace event.

- Exploiting gaps in your story. If your description of the injury shifts between the report, the doctor, and the adjuster, that inconsistency can be used against you.

- Counting on you to give up. Many valid claims are abandoned simply because the worker assumes the word “pre-existing” is the final answer.

Deadlines matter. State laws vary significantly regarding how long you have to appeal a denial or request a second opinion, and the window is sometimes measured in days. Attorneys often recommend treating any “pre-existing condition” denial as something to review immediately, because a missed appeal deadline can be far more final than the denial itself.

Approaches Injured Workers Commonly Consider

While nothing here is legal advice, the following reflects how this situation is generally navigated. Standard guidelines suggest that clear documentation is the strongest form of protection:

- Describing the change honestly. The decisive question is usually how your condition differed before and after the workplace incident, so consistency on that point tends to matter most.

- A clear treatment record. A detailed account from your treating doctor explaining how work aggravated the condition is often the most effective counter to a denial.

- Full transparency about your history. Attorneys frequently note that hiding a prior injury tends to damage credibility far more than the prior injury itself ever could.

- Knowing the rules of your state. Because aggravation standards and deadlines differ so dramatically, understanding your local rules is generally considered essential.

Federal workplace-safety standards do not govern these state benefit rules, but they establish what a safe jobsite should look like and how injuries should be recorded. You can review official employer recordkeeping and injury obligations directly at the U.S. Occupational Safety and Health Administration (OSHA).

For a broader walkthrough of how a construction claim moves from injury to resolution, our complete workers’ compensation guide breaks down each stage in plain language.

Remember: “Pre-existing condition” is an argument, not a verdict. The fact that you were not in perfect health before your injury does not erase what happened to you at work. State laws vary significantly, and the specifics of your situation always matter.

See Where You Stand Before You Accept a Denial

A denial built on your medical history can feel impossible to fight, and the stress of wondering whether you have any case at all is exhausting. Before you assume the insurer is right, it helps to understand the potential value and direction of your claim. Try the free, anonymous Benefits Estimator at HardHat Rights to get a clearer picture of your situation in minutes, with no names and no pressure. Start your free Benefits Estimator here and take the guesswork out of what comes next.

Disclaimer: This website is for informational purposes only and does not constitute legal or medical advice. The content provided is not intended to be a substitute for professional medical advice, diagnosis, or treatment. Benefit estimates are approximations based on standard state formulas and do not account for your state’s specific caps or your individual circumstances. Always consult a licensed workers’ compensation attorney in your state for legal advice, and a qualified health provider regarding any medical conditions or treatment.